Quantitative & Asset Management Toolkit: Portfolio Simulations

This section presents my perspective on Quantitative & Asset Management through two portfolio simulation projects — the Monte Carlo Portfolio Simulator and the Stock Simulator. Together, they demonstrate the ability to model uncertainty, analyze allocation strategies, and evaluate risk–return profiles across thousands of scenarios. These deliverables highlight the skills required to design robust frameworks, interpret probabilistic outcomes, and translate quantitative models into practical investment insights for decision-making.

1. Monte Carlo Portfolio Simulator

A concise profile of the Monte Carlo Portfolio Simulator, a stochastic modeling tool that generates thousands of forward-looking scenarios to assess portfolio outcomes under uncertainty. It incorporates user-defined returns, volatilities, and correlations, enabling analysis of allocation strategies, risk/return trade-offs, and goal achievement probabilities. Key outputs include fan charts, sharpe ratios, maximum drawdowns, and target success rates — making it a practical framework for portfolio construction, risk management, and client communication.

Deliverable: Interactive simulator with documentation

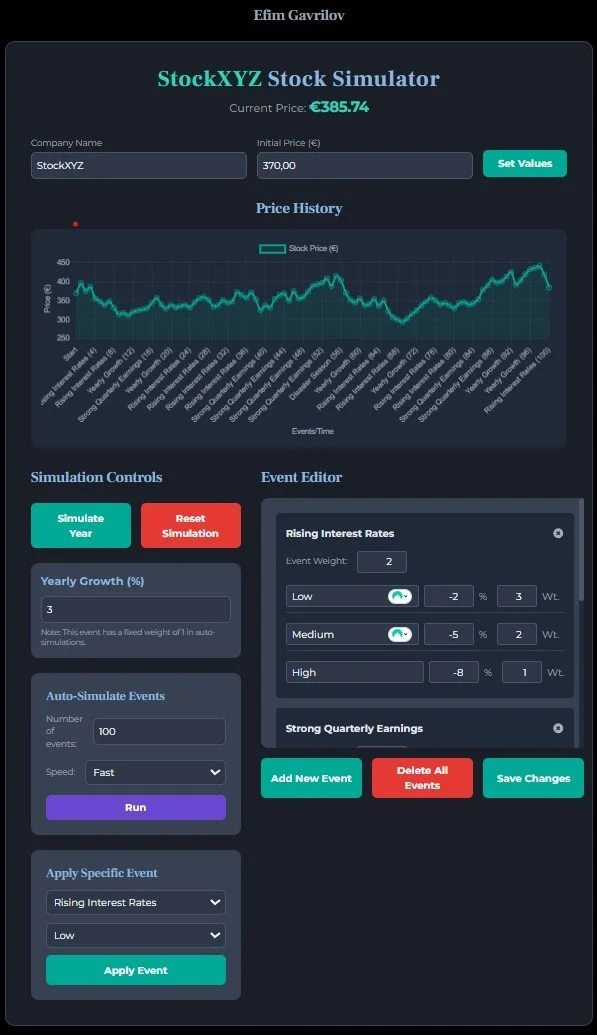

2 Stock Simulator

A concise profile of the Stock Simulator, a deterministic, event-based tool that models how individual stock prices evolve under specific scenarios. It uses an event system (e.g., earnings beats, product launches, regulatory actions) with weighted outcomes to show how news impacts valuation. Key outputs include price history charts, event impact analysis, and scenario comparisons — making it an accessible framework for teaching, equity research, and “what-if” analysis of market events.

Deliverable: Interactive simulator with documentation